MARKET ANALYSIS

System Liquidity (Nigeria)

System liquidity opened today at a surplus of ₦5.21 trillion, reflecting a decline of ₦461.94 billion compared with the previous session. The moderation in liquidity was primarily driven by the settlement of ₦235.60 billion from the prior session’s OMO auction.

Meanwhile, Deposit Money Banks (DMBs) increased their placements at the Central Bank of Nigeria (CBN)’s Standard Deposit Facility (SDF) window by ₦450.94 billion, bringing total deposits at the window to ₦5.35 trillion.

Despite the lower liquidity level, average funding costs eased by 5 basis points to 22.11%. The Open Repo Rate (OPR) remained unchanged at 22.00%, while the Overnight Rate (OVN) declined by 10 basis points to settle at 22.21%.

Projection : With an expected inflow of ₦799.13 billion from the 5-Mar-2026 NTB maturity and the 4-Mar-2026 NTB settlement, funding costs are likely to trend slightly higher in the next trading session.

Source: CBN , DPH Research

Eurobonds

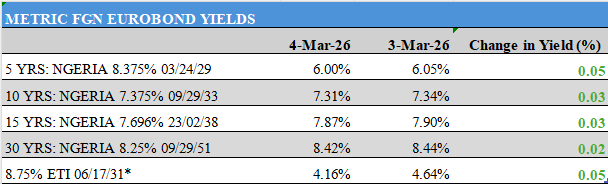

The African Eurobond market traded on a positive note, supported by investor bargain-hunting following the recent price decline. Across Nigeria’s Eurobond curve, yields trended lower.

At the short end, the Mar-2028 bond eased by 5bps to 6.00%, while the Nov-2027 declined by 4bps to 5.81%. Mid-tenors also traded bullish, with the Jan-2036 dropping 6bps to 7.68%, while the Feb-2032 and Sep-2033 shed 3bps each to 7.10% and 7.31%, respectively.

At the long end, the rally extended as the Jan-2046 and Nov-2047 eased by 4bps each to 8.36% and 8.25%, respectively, while the Sep-2053 dipped slightly by 2bps to 8.42%.

Overall, the average Nigerian Eurobond benchmark yield declined by 3bps to close at 7.22%.

Projection: We expect the market to trade mixed in the next session, as investors assess the recent yield movements alongside updates surrounding Middle East geopolitical tensions.

Source: INVESTING.COM,AIICO Capital, DPH Research

Treasury Bills

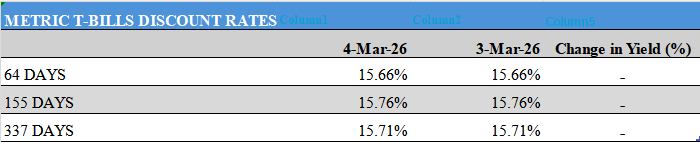

The NTB secondary market traded on a calm-to-bearish note, as market participants shifted focus to the NTB auction where the DMO offered ₦1.05 trillion across the 91-, 182-, and 364-day tenors.

Activity at the short and mid segments of the curve remained muted, with no yield movements recorded on the benchmark bills. However, the long end of the curve came under bearish pressure, as sell-side sentiment was observed on the 7-Jan-27 bill, which recorded a 41bps uptick in yield to 16.17%.

Consequently, the average benchmark yield rose by 4bps to close at 15.84%.

Projection: We expect the market to remain quiet to mildly bullish, as investors focus on submitting bids ahead of the upcoming NTB Primary Market Auction (PMA).

Source: FMDQ

FGN Bonds

The FGN bond secondary market traded on a mixed-to-bearish note amid prevailing risk-off sentiment.

At the short end of the curve, bonds traded on a mixed-to-positive note. Yield on the 23-Feb-28 bond rose by 1bp to 16.15%, while the 20-Mar-28 and 17-Apr-29 bonds eased by 1bp each to 15.95% and 15.61%, respectively.

Across the mid-tenor segment, bearish sentiment was observed on the 21-Feb-31 and 27-Apr-32 bonds, with yields rising by 46bps and 62bps to 16.23% and 16.22%, respectively. Meanwhile, long-dated bonds traded on a relatively calm note with minimal movements recorded.

Overall, the average benchmark yield increased by 6bps to close at 15.51%.

Projection: In the near term, we expect the market to retain a cautious tone as investors continue to monitor macroeconomic developments and portfolio positioning.

Source: FMDQ

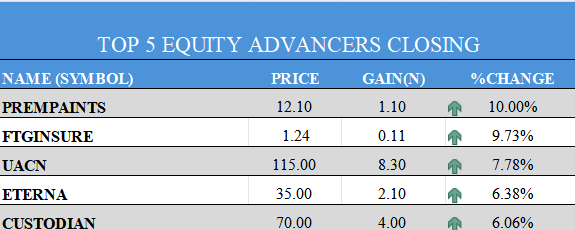

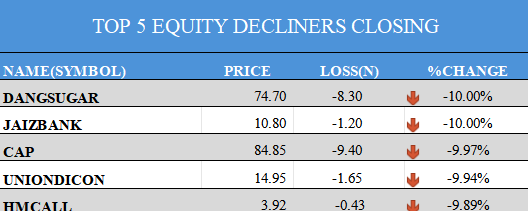

Nigerian Equities

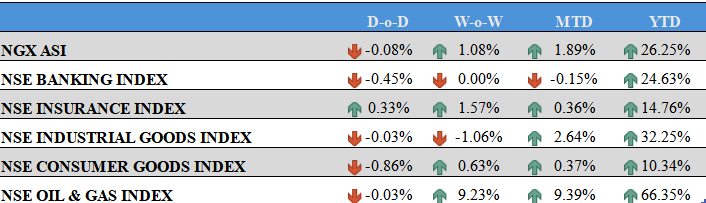

The Nigerian bourse closed the session on a negative note, as the All-Share Index (ASI) declined by 8bps, although the benchmark index remains up 26.25% year-to-date. The Pension Index also finished lower, shedding 5bps, while maintaining a stronger year-to-date return of 34.93%.

Market breadth was negative, with 22 gainers compared to 36 decliners, reflecting cautious sentiment across trading desks. PREMPAINTS (+10%) led the gainers, while DANGSUGAR (-10%) topped the losers’ chart. VERITASKAP recorded the highest trading volume at 56.42 million shares, while MTNN dominated the value chart with transactions worth ₦7.08bn.

Sector performance was broadly weak. The Banking Index declined by 45bps, pressured by losses in FCMB (-5.88%), ETI (-4.46%), ACCESSCORP (-1.89%), and WEMABANK (-0.36%), while GTCO (+0.08%) and UBA (+1.17%) posted modest gains.

The Consumer Goods Index fell by 86bps, weighed down by declines in DANGSUGAR (-10%), MCNICHOLS (-7.86%), VITAFOAM (-7.56%), INTBREW (-1.64%), HONYFLOUR (-1.53%), CHAMPION (-0.88%), and NB (-0.56%).

The Oil and Gas Index edged lower by 3bps, as JAPAULGOLD (-4.76%) and OANDO (-0.50%) declined, despite ETERNA (+6.38%) posting gains. Similarly, the Industrial Index slipped 3bps, driven by a 9.97% decline in CAP.

Trading activity weakened as total trade value declined by 14.02% to $27.18m, with notable crosses recorded in MTNN, OANDO, GTCO, ZENITHBANK, NB, and VERITASKAP.

Projection : We expect mixed market sentiment in the next session, as investors engage in profit-taking and portfolio repositioning.

Source: NGX,DPH Research

Commodities

Global oil prices were largely unchanged on Wednesday despite a volatile trading session, as renewed U.S. and Israeli strikes on Iran heightened regional tensions and disrupted shipping through the Strait of Hormuz for a fifth consecutive day, affecting key Middle East oil and gas flows.

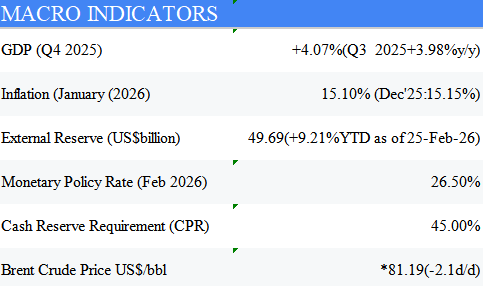

Brent crude declined slightly by 26bps (21 cents) to trade around $81.19 per barrel, while U.S. West Texas Intermediate (WTI) slipped 5bps to about $74.52 per barrel.

Meanwhile, gold prices rebounded following the previous session’s sharp decline, supported by a weaker U.S. dollar which renewed investor interest in the metal’s safe-haven appeal. Spot gold rose 91bps to approximately $5,133.85/oz, while U.S. gold futures fell 79bps to hover around $5,145.21/oz.

Projection: We expect gold to remain supported by safe-haven demand, while oil prices are likely to stay elevated amid persistent Middle East supply risks in the near term.

Source: INVESTING.COM,NBS,CBN, Bloomberg, DPH Reesearch

Foreign Exchange

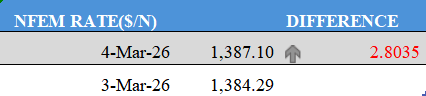

The Naira at the Nigerian Foreign Exchange Market (NFEM) remained under pressure, depreciating by 20bps (₦2.80) against the U.S. Dollar. The decline was driven by sustained demand for USD amid a broader global risk-off sentiment across emerging market assets.

During the session, the Naira traded within the ₦1,382.50/$ – ₦1,400.00/$ band before settling at ₦1,387.10/$. Meanwhile, external reserves stood at $49.69 billion as of 27-Feb-2026, reflecting a day-on-day increase of $89.14 million.

Projection: We expect the Naira to trade at relatively weaker levels in the next session, supported by prevailing demand–supply dynamics in the FX market.