MARKET ANALYSIS

System Liquidity (Nigeria)

System liquidity opened today at a surplus of ₦5.84 trillion, reflecting an increase of ₦622.34 billion from the previous session. The improvement was primarily driven by a ₦596.05 billion rise in Deposit Money Banks’ (DMBs) placements at the CBN’s Standard Deposit Facility (SDF) window, which increased to ₦5.94 trillion, alongside an inflow of ₦799.13 billion from NTB maturities. This was, however, partly offset by the ₦1.01 trillion settlement of the 4-Mar-26 NTB auction.

Despite the strong liquidity position, the average funding cost rose by 4bps to 22.14%, as the Open Repo Rate (OPR) remained unchanged at 22.00%, while the Overnight Rate (OVN) increased by 8bps to close at 22.29%.

Projection: Barring any significant funding activities, we expect funding costs to ease slightly, supported by the robust system liquidity in the banking system.

Source: CBN , DPH Research

Eurobond

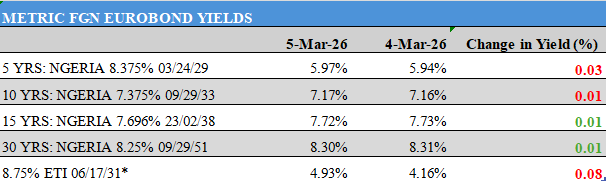

The Nigerian Sovereign Eurobond market traded on a mixed note as investors remained cautious amid persistent global uncertainties. Sentiment was influenced by rising oil prices, driven by concerns over the prolonged closure of the Strait of Hormuz following the ongoing U.S.–Iran conflict. Meanwhile, the recent NTB auction settlement of ₦622.38 billion also shaped liquidity conditions in the domestic market.

However, the firmer U.S. dollar and lingering geopolitical tensions continued to sustain a cautious risk-off tone across global markets. At the same time, the latest U.S. labour market data showed initial jobless claims holding steady at 213,000, reflecting ongoing labour market resilience and helping stabilize broader sentiment.

Consequently, the average benchmark yield held steady at 7.11%.

Projection: We expect the market to trade mixed in the near term, amid the recent yield uptick and evolving developments surrounding Middle-East tensions.

Source: INVESTING.COM,AIICO Capital, DPH Research

Treasury Bills

The NTB secondary market traded on a mixed and cautious note as investors assessed the outcome of the previous day’s NTB Primary Market Auction (PMA). The DMO allotted about ₦1.01 trillion across the 91-day, 182-day, and 364-day tenors from total subscriptions of ₦2.34 trillion, reflecting strong investor demand, particularly for the 364-day bill. The one-year paper cleared at 16.73%, representing an 83bps increase from the previous stop rate.

Secondary market activity remained subdued, though mild upward repricing was observed across some maturities. Notably, the 3-Sep-26 bill rose 45bps to 16.15%. Meanwhile, the newly issued 4-Mar-27 bill saw limited demand, closing at 16.45%. Consequently, the average benchmark rate increased by 8bps to 15.92%.

Projection: We expect the market to trade in line with prevailing system liquidity conditions.

Source: FMDQ

FGN Bonds

The FGN bond secondary market maintained a bearish bias, extending the weak sentiment from the previous session as investors reacted to the outcome of the NTB Primary Market Auction (PMA). The auction results prompted market participants to reassess their positions amid signals of a potential upward adjustment in yields.

Market activity remained relatively subdued, with limited transactions concentrated around the mid-segment of the yield curve. By the close of trading, the FGN 2031 and FGN 2032 bonds were quoted at 16.26% (+5bps) and 16.23% (+1bp), respectively.

Overall, the average benchmark yield remained unchanged at 15.51%, indicating a largely stable close despite the prevailing cautious sentiment.

Projection: In the near term, we expect the market to maintain a cautious tone as investors continue to monitor liquidity conditions and yield direction.

Source: FMDQ

Nigerian Equities

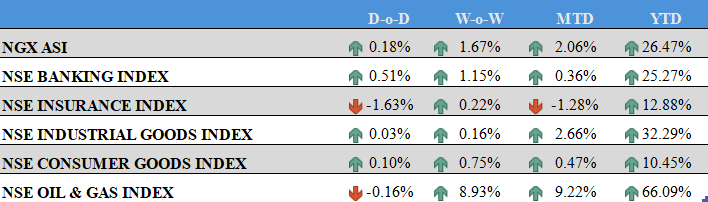

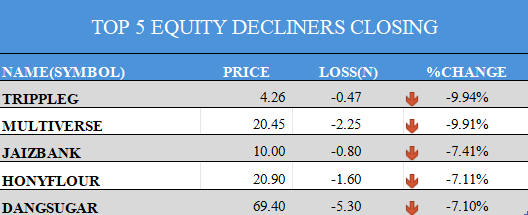

The Nigerian equities market closed Thursday’s trading session on a positive note, as the NGX All-Share Index (ASI) advanced by 18bps, supported by gains in large-cap stocks such as MTN Nigeria Communications Plc (MTNN) and Nestlé Nigeria Plc (NESTLE). Despite the upward movement in the benchmark index, market breadth closed negative, with 32 gainers against 37 decliners.

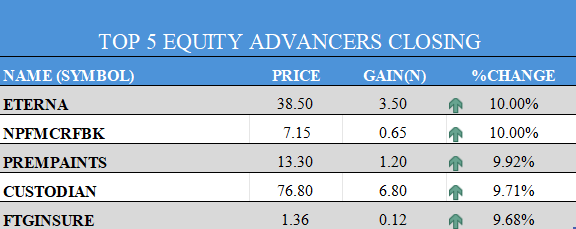

NPF Microfinance Bank Plc (NPFMCRFBK) and Eterna Plc (ETERNA) led the gainers’ chart with 10% appreciation each, while Tripple Gee and Company Plc (TRIPPLEG) recorded the largest loss of the session, declining by 9.94%.

In terms of trading activity, Guaranty Trust Holding Company Plc (GTCO) topped both the volume and value charts, with 45.47 million shares traded worth ₦5.41 billion.

Sectoral Performance

Banking Index: Gained 51bps, driven by price increases in Stanbic IBTC Holdings Plc (STANBIC) (+5.56%), Zenith Bank Plc (ZENITHBANK) (+1.2%), FCMB Group Plc (FCMB) (+0.39%), and United Bank for Africa Plc (UBA) (+0.11%), while Fidelity Bank Plc (FIDELITYBK) (-1%) and Wema Bank Plc (WEMABANK) (-2.7%) declined.

Consumer Goods Index: Advanced 10bps, supported by gains in Nestlé Nigeria Plc (NESTLE) (+4.84%), Vitafoam Nigeria Plc (VITAFOAM) (+3.91%), Cadbury Nigeria Plc (CADBURY) (+0.29%), and Champion Breweries Plc (CHAMPION) (+0.29%), although International Breweries Plc (INTBREW), McNichols Plc (MCNICHOLS), Guinness Nigeria Plc (GUINNESS), Dangote Sugar Refinery Plc (DANGSUGAR), and Honeywell Flour Mills Plc (HONYFLOUR) closed lower.

Oil & Gas Index: Declined 16bps, pressured by losses in Oando Plc (OANDO) (-4%), although Japaul Gold and Ventures Plc (JAPAULGOLD) (+2.63%) and Eterna Plc (ETERNA) (+10%) recorded gains.

Industrial Index: Rose marginally by 3bps, supported by Chemical and Allied Products Plc (CAP) (+8.72%) and Dangote Cement Plc (DANGCEM) (+0.01%), while Cutix Plc (CUTIX) and Tripple Gee and Company Plc (TRIPPLEG) recorded losses.

Trading activity weakened as total trade value declined by 26.83% to $19.94 million, with notable cross trades recorded in MTNN, GTCO, and NESTLE.

Projection: We expect mixed market sentiment in the next session, as profit-taking and portfolio repositioning continue to influence trading activity.

Source: NGX,DPH Research

Commodities

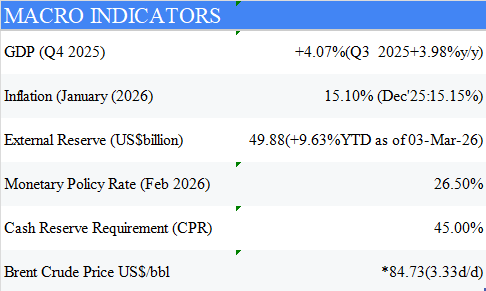

Global oil prices settled sharply higher on Thursday, extending the recent rally as the escalating tensions between the United States, Israel, and Iran disrupted supply chains and shipping routes across the Middle East, prompting some major regional producers to scale back output. Brent Crude rose by 4.09% ($3.33) to trade around $84.73 per barrel, while West Texas Intermediate (WTI) advanced 7.49% to approximately $80.25 per barrel.

Conversely, Gold prices reversed the previous session’s gains, falling to a two-day low as stronger U.S. Treasury yields and a firmer United States Dollar weighed on the precious metal. The pressure was largely driven by robust U.S. labour market data, which reinforced expectations of sustained higher interest rates. Spot gold declined by 114bps to $5,077.43/oz, while U.S. gold futures fell 92bps to hover around $5,087.66/oz.

Projection: We expect oil prices to remain supported in the near term due to supply concerns linked to the escalating Iran conflict, while gold may remain under pressure amid a stronger U.S. dollar and elevated Treasury yields.

Source: INVESTING.COM,NBS,CBN, Bloomberg, DPH Reesearch

Foreign Exchange

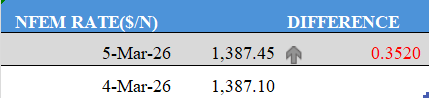

The Nigerian Naira at the Nigerian Foreign Exchange Market (NFEM) remained under pressure, depreciating marginally by 3bps (₦0.35) against the United States Dollar. The depreciation was primarily driven by limited FX supply at the start of the trading session, although liquidity conditions improved slightly towards the close.

During the session, the Naira traded within the ₦1,382.00/$ – ₦1,388.00/$ band, before settling at ₦1,387.45/$ by the close of trading. Meanwhile, external reserves were recorded at $49.88 billion as of 3-Mar-2026, reflecting an increase of $189.14 million compared to the level reported last Friday.

Projection: We expect the Naira to trade at relatively weaker levels in the next session, supported by prevailing demand–supply dynamics in the FX market.