MARKET ANALYSIS

System Liquidity (Nigeria)

System liquidity opened the session in a surplus position of ₦4.39 trillion, representing an increase of ₦682.39 billion compared to the previous session. The improvement was largely driven by higher Deposit Money Banks (DMBs) placements at the CBN’s Standard Deposit Facility (SDF) window, which rose from ₦3.62 trillion to ₦4.32 trillion.

Despite the liquidity surplus, average funding costs edged higher by 9bps to 22.18%. The Open Repo Rate (OPR) remained unchanged at 22.00%, while the Overnight Rate (OVN) advanced by 18bps to close at 22.35%, indicating sustained tightness in interbank funding conditions.

Overall, money market rates continue to reflect cautious liquidity management and persistent demand for short-term funds.

Projection : Barring any significant funding activities or liquidity injections, funding costs are likely to remain elevated in the near term.

Source: CBN , DPH Research

Eurobonds

The African Eurobond market traded on a bearish note amid heightened risk aversion. The uptick in yields was driven by surging oil prices around the $78/bbl level following escalating tensions in the Middle East, alongside mixed global cues including softer U.S. inflation at 2.4%, but intensified geopolitical risks after reported U.S.–Israel strikes on Iran.

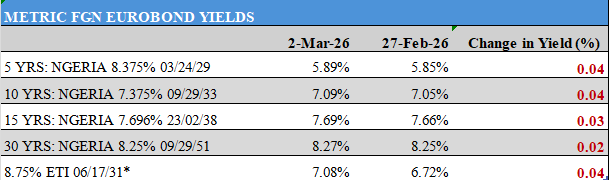

Across Nigeria’s Eurobond curve, yields trended higher amid broad-based sell-offs.

At the short end, the Nov-2027 maturity rose by 7bps to 5.42%, while Sep-2028 and Mar-2029 increased by 6bps and 4bps to 5.66% and 5.89%, respectively.

Mid-tenors also weakened, with Feb-2030 and Jan-2031 climbing by 12bps and 11bps to 6.30% and 6.67%, respectively.

The long end extended the bearish move as Jan-2036 advanced by 5bps to 7.55%, while Feb-2038 rose by 3bps to 7.69%.

Overall, the average Nigerian Eurobond benchmark yield widened by 5bps to close at 7.06%, reflecting sustained risk repricing across the curve.

Projection : We expect the market to trade in line with oil price volatility and macroeconomic updates, with investor sentiment remaining highly sensitive to geopolitical developments and global risk appetite.

Source: INVESTING.COM,AIICO Capital, DPH Research

Treasury Bills

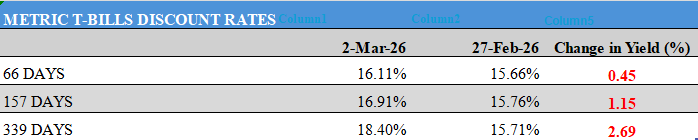

The NTB secondary market traded on a bearish note, with yields expanding sharply amid sustained selling pressure and investor repositioning.

Across the curve, short-end bills recorded moderate increases as nearby maturities closed weaker. In the mid- to longer-tenor segment, yields climbed more aggressively, reflecting intensified sell-offs and reduced appetite for duration.

Notably, the 04-Feb-27 bill posted a significant uptick of 269bps to 18.40%, underscoring pronounced pressure at the far end of the curve. As a result, the average benchmark rate widened by 143bps to close at 17.24%, indicating broad-based repricing across maturities.

Overall, market activity suggests defensive positioning as participants adjust to evolving liquidity conditions and rate expectations.

Projection : We expect the market to maintain a cautious tone in the near term, with yields likely to remain elevated amid continued investor repricing and funding considerations.

Source: FMDQ

FGN Bonds

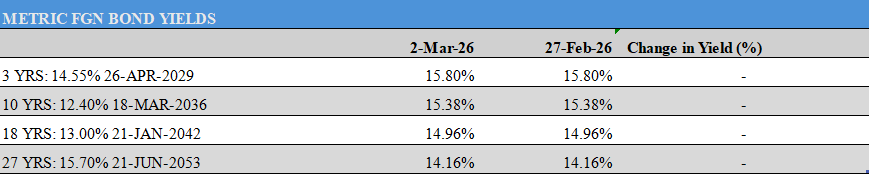

The FGN bond secondary market traded on a stable note day-on-day, with yields largely unchanged amid balanced trading activity and sustained investor confidence in the naira fixed-income curve.

Across the curve, short- to mid-tenor bonds remained mostly flat as maturities closed steady or recorded only marginal movements. Notably, the 17-Mar-27 bond ticked up by 1bp to 16.06%, while the 20-Mar-27 eased by 2bps to 15.93%. At the longer end, the 21-Jun-38 maturity dipped by 1bp to 15.21%, reflecting selective repositioning at specific points on the curve.

The broadly flat performance underscores steady demand for high real yields, supported by the CBN’s recent 50bps MPR cut, improved FX stability, moderating inflation trends, and strong participation at recent primary auctions.

Overall, the average benchmark yield remained unchanged at 15.42%, highlighting the market’s consolidation phase.

Projection : In the near term, we expect the market to retain a cautious tone, with investors likely to remain selective as they assess liquidity conditions, inflation dynamics, and further policy signals.

Source: FMDQ

Nigerian Equities

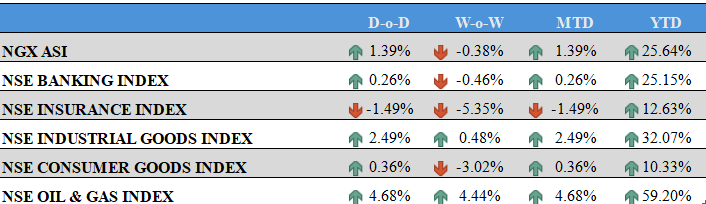

The Nigerian bourse closed the session on a positive note, as the All-Share Index (ASI) advanced by 139bps, lifting the year-to-date (YTD) return to 25.64%. The Pension Index also strengthened, gaining 142bps and pushing its YTD return to 33.98%.

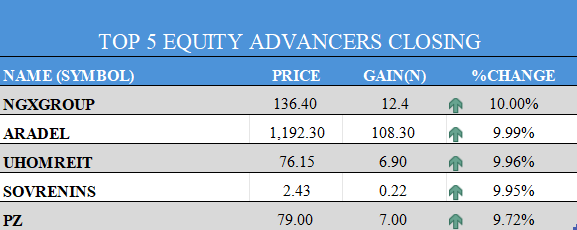

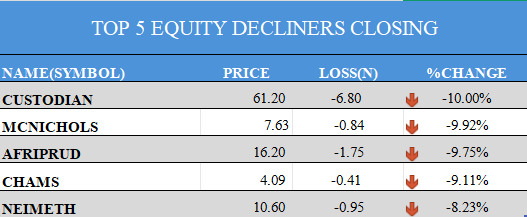

Market breadth was neutral, with 31 gainers and 31 losers. NGXGROUP (+10.00%) led the advancers, while CUSTODIAN (-10.00%) topped the losers’ chart.

Trading activity was mixed. FTGINSURE recorded the highest volume at 109.07 million shares, while ARADEL dominated the value chart with ₦6.09bn worth of transactions. Overall trade value rose by 1.9% to $25.34m, supported by notable cross trades in DANGCEM, ARADEL, and MTNN.

Sector Performance

Sectoral performance was broadly positive:

Banking Index gained 26bps, driven by advances in WEMABANK (+3.52%), STANBIC (+3.28%), ZENITHBANK (+1.04%), GTCO (+0.81%), and FIDELITYBK (+0.25%), which offset declines in ACCESSCORP (-2.08%), FCMB (-2.88%), and UBA (-3.28%).

Consumer Goods Index added 36bps, supported by gains in PZ (+9.72%), INTBREW (+3.10%), HONYFLOUR (+0.66%), and NB (+0.06%), despite losses in DANGSUGAR (-2.35%), CHAMPION (-5.56%), and MCNICHOLS (-9.92%).

Oil and Gas Index surged by 468bps, driven by strong rallies in ARADEL (+9.99%), OANDO (+9.33%), and JAPAULGOLD (+3.37%).

Industrial Index advanced by 249bps, following gains in DANGCEM (+3.97%) and WAPCO (+3.75%), although declines in CUTIX (-2.62%), AUSTINLAZ (-4.99%), and CAP (-5.05%) tempered the upside. Earnings releases from DANGCEM and BUACEMENT were noted during the session.

Overall, the positive close was underpinned by strong buying interest in oil & gas and industrial heavyweights, alongside selective positioning in banking names.

Projection : We expect mixed market performance in the next session as participants engage in profit-taking and portfolio repositioning activities.

Source: NGX,DPH Research

Commodities

Global oil and gas prices surged on Monday following Israeli and U.S. strikes on Iran, alongside retaliatory actions by Tehran, which led to the shutdown of key oil and gas facilities across parts of the Middle East and disrupted shipping activities through the strategic Strait of Hormuz.

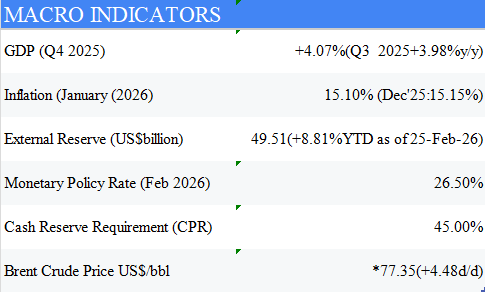

Brent crude jumped 6.15% (or $4.48) to trade around $77.35 per barrel, while U.S. West Texas Intermediate (WTI) climbed 5.74% from Friday’s close to approximately $70.87 per barrel. The sharp rally reflects heightened supply risk premiums amid fears of prolonged disruptions in a region that accounts for a significant share of global energy exports.

Similarly, safe-haven gold strengthened as investors reacted to the risk of an extended geopolitical conflict. Spot gold advanced by 104bps to around $5,332.85/oz, while U.S. gold futures rose by 110bps to hover near $5,305.74/oz, supported by increased demand for defensive assets.

Overall, commodity markets remain highly sensitive to geopolitical developments, particularly those affecting energy infrastructure and critical shipping routes.

Projection : Oil prices are likely to remain firm and potentially push higher as markets continue to price in supply disruption risks. Meanwhile, gold is expected to stay supported amid escalating hostilities and persistent global uncertainty.

Source: INVESTING.COM,NBS,CBN, Bloomberg, DPH Reesearch

Foreign Exchange

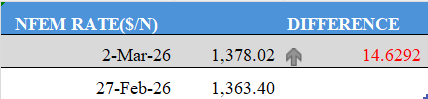

The Naira at the Nigerian Foreign Exchange Market (NFEM) extended its negative run this week, depreciating by 27bps (₦3.70) against the U.S. Dollar. The weakness was primarily driven by sustained USD demand pressure, which outweighed inflows from Foreign Portfolio Investors (FPIs) and local market participants.

During the session, the Naira traded within a band of ₦1,356.50/$ to ₦1,362.90/$ before settling at ₦1,359.82/$, reflecting persistent demand–supply imbalance in the market.

Meanwhile, Nigeria’s external reserves rose to $49.51 billion as of 25-Feb-2026, representing a day-on-day increase of $115.96 million, suggesting continued FX inflows despite spot market pressure.

Overall, FX dynamics remain influenced by elevated demand conditions, capital flow trends, and liquidity positioning within the system.

Projection : We expect the Naira to trade at relatively weaker levels in the next session, supported by prevailing demand pressures and current supply dynamics in the FX market.