Friday, 27 February 2026

MARKET ANALYSIS

System Liquidity (Nigeria)

System liquidity opened the session in surplus at ₦2.68 trillion, representing a decline of ₦850.64 billion from the previous day. The moderation was primarily driven by a reduction in Deposit Money Banks’ (DMBs) placements at the CBN’s Standard Deposit Facility (SDF), which declined from ₦3.97 trillion to ₦3.71 trillion. This was largely offset by the ₦1.11 trillion settlement from the OMO auction conducted the previous day across the 6-, 104-, and 167-day tenors.

As a result, average funding costs edged higher by 5bps to 22.13%. The Open Repo Rate (OPR) remained unchanged at 22.00%, while the Overnight Rate (OVN) increased by 10bps to 22.25%.

Projection : Barring any significant liquidity injections or funding activities, we expect funding costs to remain elevated in the near term.

Source: CBN , DPH Research

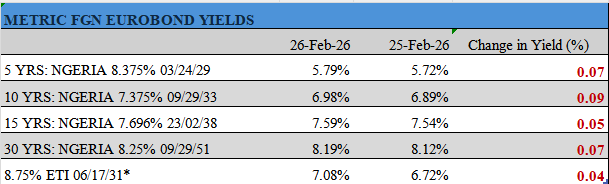

Eurobonds

The African Eurobond market traded on a mildly bearish note amid cautious investor sentiment. The uptick in yields reflected continued oil price volatility around the $70–71/bbl range, alongside mixed global cues including softer U.S. inflation data and persistent geopolitical tensions in the Middle East. Across Nigeria’s Eurobond curve, yields moved higher.

At the short end, the Nov-2027 bond rose by 1bp to 5.21%, while Sep-2028 and Mar-2029 advanced by 3bps and 7bps to 5.49% and 5.79%, respectively.

Mid-tenors also weakened, with Feb-2030 and Jan-2031 climbing 8bps and 9bps to 6.13% and 6.46%, respectively.

At the long end, the bearish momentum persisted as Jan-2036 increased by 11bps to 7.44%, while Dec-2034 rose by 8bps to 7.27%.

Overall, the average Nigerian Eurobond benchmark yield widened by 6bps to close at 6.94%, reflecting broad-based risk repricing across the curve.

Projection : We expect the market to trade in line with oil price volatility and incoming macroeconomic developments.

Source: INVESTING.COM,AIICO Capital, DPH Research

Treasury Bills

The NTB secondary market traded on a largely stable note, with yields holding firm across most maturities amid muted activity and balanced demand–supply dynamics.

Across the curve, short- to mid-tenor bills remained unchanged as maturities closed steady. Similarly, mid- to long-end bills maintained prior levels, reflecting limited directional bias and cautious positioning by market participants.

Notably, the 04-Feb-27 bill recorded a marginal uptick of 23bps to 15.68%, indicating selective interest at the far end of the curve. Consequently, the average benchmark rate inched higher by 2bps to close at 15.85%.

Overall, trading activity suggests a wait-and-see approach, with investors maintaining defensive positioning while monitoring liquidity conditions and primary market signals.

Projection : We expect the market to maintain a cautious tone in the near term.

Source: FMDQ

FGN Bonds

The FGN bond secondary market traded on a mixed note, as selective buying interest across segments of the curve was offset by pockets of mild sell pressure, while several benchmark maturities closed unchanged.

At the short end, the 20-Mar-27 and 21-Feb-31 maturities edged lower by 1bp apiece to 15.96% and 15.78%, respectively, while other short-dated instruments held steady.

In the mid-segment, the 17-Apr-29 bond weakened, with its yield rising by 11bps to 16.01%. Conversely, the 27-Apr-32 and 15-May-33 maturities rallied, posting notable yield compressions of 18bps and 14bps to close at 15.60% and 15.59%, respectively, reflecting targeted demand within that bucket.

Further along the curve, the 21-Feb-34 and 18-Jul-34 bonds recorded yield increases of 7bps and 19bps to settle at 15.59% and 15.68%, respectively, while longer-dated instruments remained largely unchanged.

Overall, despite the mixed performance across individual maturities, the average benchmark yield declined by 29bps to close at 15.44%, suggesting modest net buying bias across the broader curve.

Projection: We expect trading to remain selective in the near term, with investors focusing on liquidity conditions, inflation expectations, and upcoming supply dynamics for clearer directional cues.

Source: FMDQ

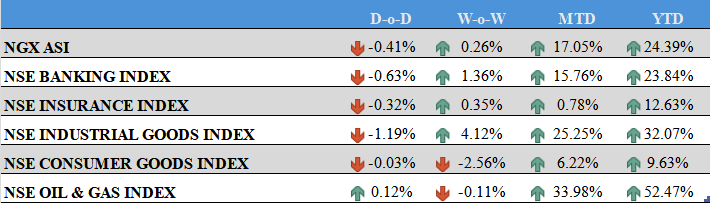

Nigerian Equities

The Nigerian bourse closed the session on a negative note, as the All-Share Index (ASI) declined by 41bps. Nonetheless, the market retained a solid 24.39% year-to-date (YTD) return. Similarly, the Pension Index shed 56bps on the day but continues to reflect a strong 31.91% YTD gain.

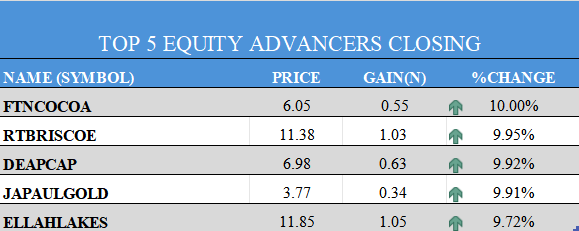

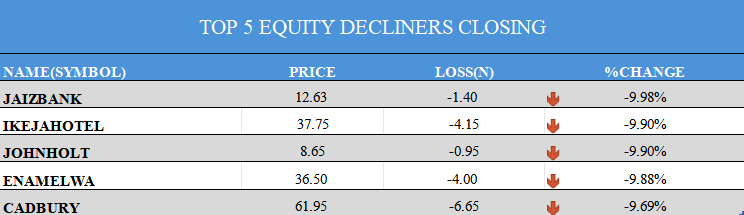

Market breadth was mildly negative, with 30 gainers against 37 decliners. FTNCOCOA (+10.00%) led the advancers, while IKEJAHOTEL (-9.90%) topped the losers’ chart.

Trading activity was mixed. JAPAULGOLD recorded the highest volume traded at 73.25 million shares, while ZENITHBANK dominated the value chart with ₦4.06bn worth of transactions. Overall trade value declined by 32.83% to $22.33m, reflecting softer participation and mild profit-taking activity.

Sector Performance

Sectoral performance was broadly weak:

- Banking Index declined by 63bps, pressured by losses in UBA (-3.27%), ZENITHBANK (-2.20%), ACCESSCORP (-1.50%), WEMABANK (-1.10%), FCMB (-1.09%), FIDELITYBK (-0.98%), and GTCO (-0.76%).

- Consumer Goods Index edged lower by 3bps, weighed down by CADBURY (-9.69%), DANGSUGAR (-3.51%), PZ (-1.55%), HONYFLOUR (-0.43%), and NB (-0.06%). Gains in UNILEVER (+5.44%), VITAFOAM (+5.78%), and CHAMPION (+9.38%) helped moderate the decline.

- Oil and Gas Index advanced by 12bps, supported by JAPAULGOLD (+9.91%) and OANDO (+1.75%).

- Industrial Index dipped by 119bps, driven largely by WAPCO (-8.21%), despite strength in CUTIX (+8.74%).

Overall sentiment remained cautious as selective profit-taking across key sectors offset isolated buying interest.

Source: NGX,DPH Research

Commodities

Global oil prices advanced by nearly $1 on Thursday as investors awaited the outcome of a third round of talks between the United States and Iran regarding the latter’s nuclear program.

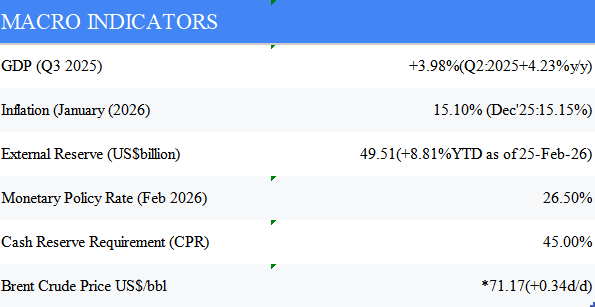

Brent crude rose by 48bps (34 cents) to hover around $71.17 per barrel, while U.S. West Texas Intermediate (WTI) gained 32bps to trade near $65.63 per barrel. The gains reflect geopolitical risk premium returning to the market amid uncertainty surrounding potential supply disruptions.

Conversely, gold traded mixed as investors weighed concerns that tariffs could fuel inflationary pressures, while persistent geopolitical tensions between the United States and Iran sustained safe-haven demand.

Spot gold edged up 2bps to approximately $5,172.26/oz, while U.S. gold futures declined by 45bps to hover around $5,202.54/oz.

Overall, commodity markets remain highly sensitive to geopolitical developments, inflation expectations, and policy signals from major economies.

Projection ; We expect metals to trade in line with macroeconomic developments, particularly inflation data and policy guidance, while oil prices may continue to face structural supply headwinds despite heightened geopolitical tensions.

Source: INVESTING.COM,NBS,CBN, Bloomberg, DPH Reesearch

Foreign Exchange

The Naira at the Nigerian Foreign Exchange Market (NFEM) extended its negative run this week, depreciating by 27bps (₦3.70) against the U.S. Dollar. The weakness was primarily driven by sustained USD demand pressure, which outweighed inflows from Foreign Portfolio Investors (FPIs) and local market participants.

During the session, the Naira traded within a band of ₦1,356.50/$ to ₦1,362.90/$ before settling at ₦1,359.82/$, reflecting persistent demand–supply imbalance in the market.

Meanwhile, Nigeria’s external reserves rose to $49.51 billion as of 25-Feb-2026, representing a day-on-day increase of $115.96 million, suggesting continued FX inflows despite spot market pressure.

Overall, FX dynamics remain influenced by elevated demand conditions, capital flow trends, and liquidity positioning within the system.

Projection : We expect the Naira to trade at relatively weaker levels in the next session, supported by prevailing demand pressures and current supply dynamics in the FX market.